Customer Loan Default Prediction

Predictive modeling

The goal is to build a model that predicts a probability that a given customer will default on a loan. A customer profile consists of a list of bank transactions preceding the loan request. Each transaction is either a debit (money going out of account, negative values) or credit (money coming into account, positive values).

Customer profile (attributes, 15000 customers total):

Id: id of each customerdates: dates of each transactiontransaction_amount: numpyarray of credits and debits, length varies across different customers (predictions will be primarily based oninformation inthis array)days_before_request_days: before loan request for each transactionloan_amount: amount loaned to customer by bankloan_date: date of loan

Outcome:

isDefault: the customer pay back (isDefault=0) or not pay back (isDefault=1)

isDefault is given for the first 10000 customers. The job is to assign a probability to isDefault for the remaining 5000 customers. Train the model on the training data (instances 0-9999) and make predictions on the test data (instances 10000-14,999). The test data is the same format as training data, except it does not contain the isDefault column. The data is available here. The data can be loaded from dataset_new.pkl in Python using:

import pandas as pd

data = pd.read_pickle('dataset_new.pkl')

Construct features:

import numpy as np

from datetime import datetime

def mk_data(data, num):

features = np.zeros((data.shape[0], 16*10*3+1))

targets = np.zeros(num)

for i in range(len(data)):

dates = data[1][i][1]

trxn_amount = data[2][i][1]

loan_amount = data[4][i][1]

loan_date = data[5][i][1]

if i < num:

targets[i] = data[6][i][1]

features[i][-1] = loan_amount

trxn_grps = dict()

for j in range(len(trxn_amount)):

amount = trxn_amount[j][0]

days = (datetime.strptime(loan_date, '%Y-%m-%d') - datetime.strptime(dates[j], '%Y-%m-%d')).days

day_idx = min(days//10, 9)

if amount <= -50000:

amount_idx = 0

elif amount > -50000 and amount <= -20000:

amount_idx = 1

elif amount > -20000 and amount <= -10000:

amount_idx = 2

elif amount > -10000 and amount <= -5000:

amount_idx = 3

elif amount > -5000 and amount <= -2000:

amount_idx = 4

elif amount > -2000 and amount <= -1000:

amount_idx = 5

elif amount > -1000 and amount <= -500:

amount_idx = 6

elif amount > -500 and amount <= 0:

amount_idx = 7

elif amount > 0 and amount <= 500:

amount_idx = 8

elif amount > 500 and amount <= 1000:

amount_idx = 9

elif amount > 1000 and amount <= 2000:

amount_idx = 10

elif amount > 2000 and amount <= 5000:

amount_idx = 11

elif amount > 5000 and amount <= 10000:

amount_idx = 12

elif amount > 10000 and amount <= 20000:

amount_idx = 13

elif amount > 20000 and amount <= 50000:

amount_idx = 14

else:

amount_idx = 15

idx = day_idx * 16 + amount_idx

if idx not in trxn_grps:

trxn_grps[idx] = []

trxn_grps[idx].append(amount)

for day_idx in range(9, -1, -1):

for amount_idx in range(15, -1, -1):

idx = day_idx * 16 + amount_idx

if idx in trxn_grps and len(trxn_grps[idx]) > 0:

amounts = trxn_grps[idx]

if day_idx == 9:

features[i][idx*3] = 0

features[i][idx*3+1] = len(amounts)

features[i][idx*3+2] = np.sum(amounts)

else:

features[i][idx*3] = 0

features[i][idx*3+1] = features[i][(idx+1)*3+1] + len(amounts)

features[i][idx*3+2] = features[i][(idx+1)*3+2] + np.sum(amounts)

else:

if day_idx == 9:

features[i][idx*3] = 1

features[i][idx*3+1] = 0

features[i][idx*3+2] = 0

else:

features[i][idx*3] = features[i][(idx+1)*3] + 1

features[i][idx*3+1] = features[i][(idx+1)*3+1]

features[i][idx*3+2] = features[i][(idx+1)*3+2]

return features, targets

Train test split:

x_train = features[:10000, :]

x_val = features[10000:10500, :]

x_test = features[10000:, :]

y_train = targets[:10000]

y_val = targets[10000:]

from sklearn.ensemble import GradientBoostingClassifier

clf = GradientBoostingClassifier(n_estimators=160)

from sklearn.model_selection import StratifiedKFold

from sklearn.metrics import roc_curve, auc

tprs = np.zeros([10,100])

aucs = np.zeros([10])

mean_fpr = np.linspace(0, 1, 100)

cv = StratifiedKFold(n_splits=10)

i=0

for train, test in cv.split(x_train, y_train):

probas_ = clf.fit(x_train[train], y_train[train]).predict_proba(x_train[test])

fpr, tpr, thresholds = roc_curve(y_train[test], probas_[:, 1])

tprs[i,:] = np.interp(mean_fpr, fpr, tpr)

roc_auc = auc(fpr, tpr)

aucs[i] = roc_auc

i+=1

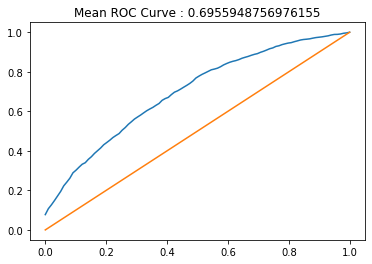

import matplotlib.pyplot as plt

plt.plot(mean_fpr,np.mean(tprs,axis=0))

plt.plot([0,1],[0,1])

plt.title('Mean ROC Curve : '+str(np.mean(aucs)))

plt.show()

Fit the model:

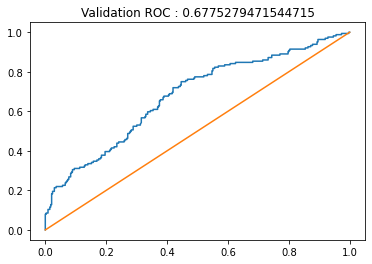

clf.fit(x_train, y_train)

probas_=clf.predict_proba(x_val)

fpr, tpr, thresholds = roc_curve(y_val, probas_[:, 1])

roc_auc = auc(fpr, tpr)

plt.plot(fpr,tpr)

plt.plot([0,1],[0,1])

plt.title('Validation ROC : '+str(roc_auc))

plt.show()

Validation ROC curve of the model:

Top 5 most important features:

print(clf.feature_importances_.argsort()[-5:][::-1])

[480 21 24 27 368]

Make prediction using clf.predict_proba(x_test)[:, 1].